What's Typically Covered

Standard Delaware homeowners policies generally cover sudden, accidental water damage: a burst supply line, a failed water heater, an overflowing appliance, or a storm-driven roof leak. These events are considered unexpected and outside your control, which is exactly what homeowners insurance is designed to address.

What's Typically Excluded

Gradual leaks that built up over weeks or months, rising floodwater from a storm or overflowing waterway, and mold beyond a policy's coverage cap are commonly excluded from standard policies. Rising floodwater specifically requires a separate NFIP or private flood policy, since Wilmington's exposure to Christina River and Brandywine Creek flooding falls outside typical homeowners coverage. Our flood damage restoration page covers how we handle these events regardless of which policy applies.

Delaware's Claims-Handling Timeline

Delaware's insurance code, 18 Del. C. § 2304(16)(f) and the related administrative regulations at 18 Del. Admin. Code § 902, requires insurers to acknowledge claim communications within 15 working days, begin investigating within 10 working days, and affirm or deny coverage within 30 days after proof-of-loss documents are submitted. Unlike some states, Delaware doesn't set a fixed number of days for payment after acceptance, instead requiring a good-faith standard of prompt, fair, and equitable settlement once liability is reasonably clear.

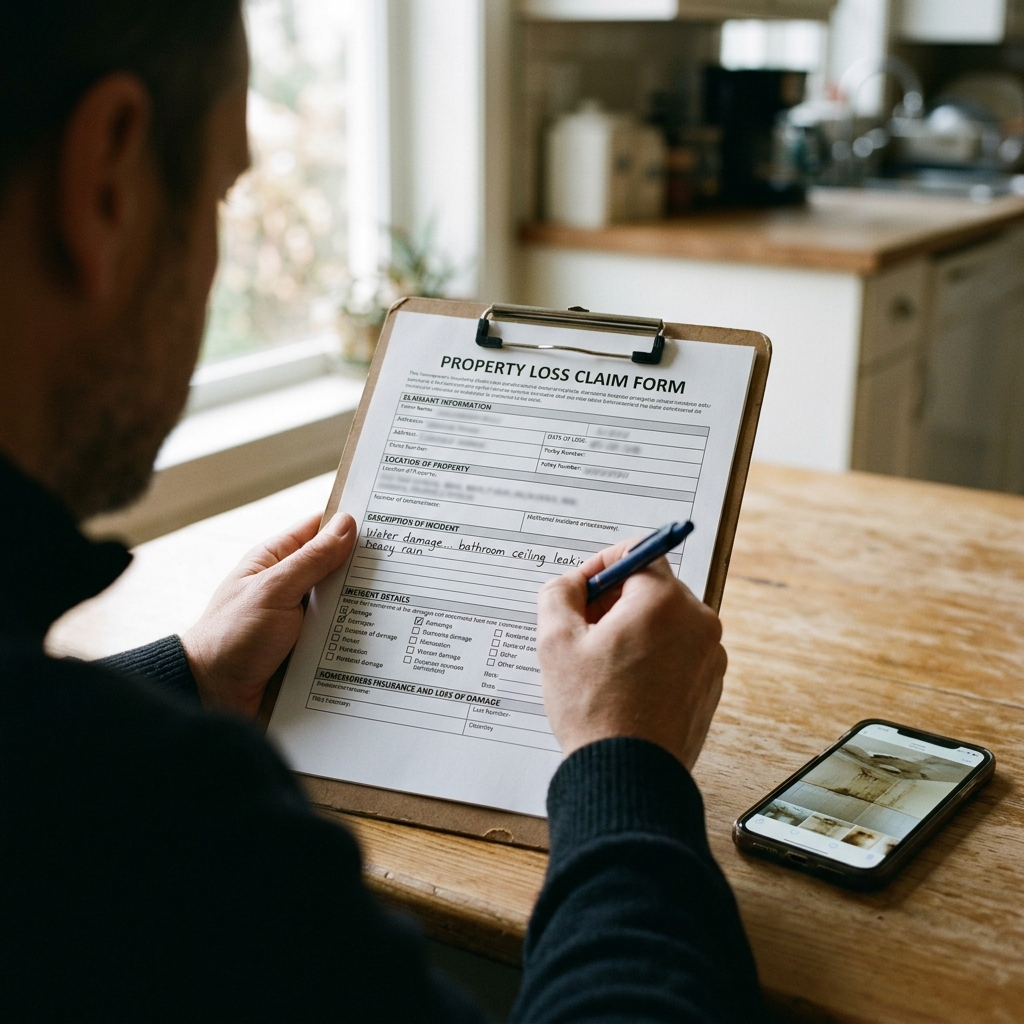

Why Documentation Matters More Than You'd Think

Your insurer's response timeline only moves forward once you've actually filed a complete claim with proof of loss. Moisture readings, photos of the damage and its source, and a clear narrative of what happened all speed up that 30-day determination window. Our water mitigation service produces exactly this kind of documentation as part of the standard cleanup process, not as an extra step.

What to Do in the First Hour After Water Damage

Document the damage with photos before moving anything, note the time you discovered it, and call a restoration company and your insurer as soon as reasonably possible. Most policies include a duty to mitigate further damage, and acting promptly protects both your home and your claim.

When Coverage Gets Complicated

Basement flooding is one of the more commonly disputed categories, since it can stem from a covered burst pipe, an excluded gradual seepage issue, or excluded rising floodwater, sometimes all in the same event. Our basement water damage team documents the specific source so your adjuster has clear evidence for which category applies.

Not sure if your Wilmington water damage is covered? Call us at (302) 267-7950. We'll document the damage regardless, which protects your claim no matter how the coverage question resolves.